Indonesia controls a resource that the entire global automotive industry is scrambling to secure. The country holds some of the largest nickel reserves on the planet, and nickel is the primary mineral driving the lithium-ion battery supply chain behind electric vehicles. On paper, Indonesia should be positioned as a cornerstone of the global clean energy transition. The reality of how that nickel is being processed tells a sharply different story.

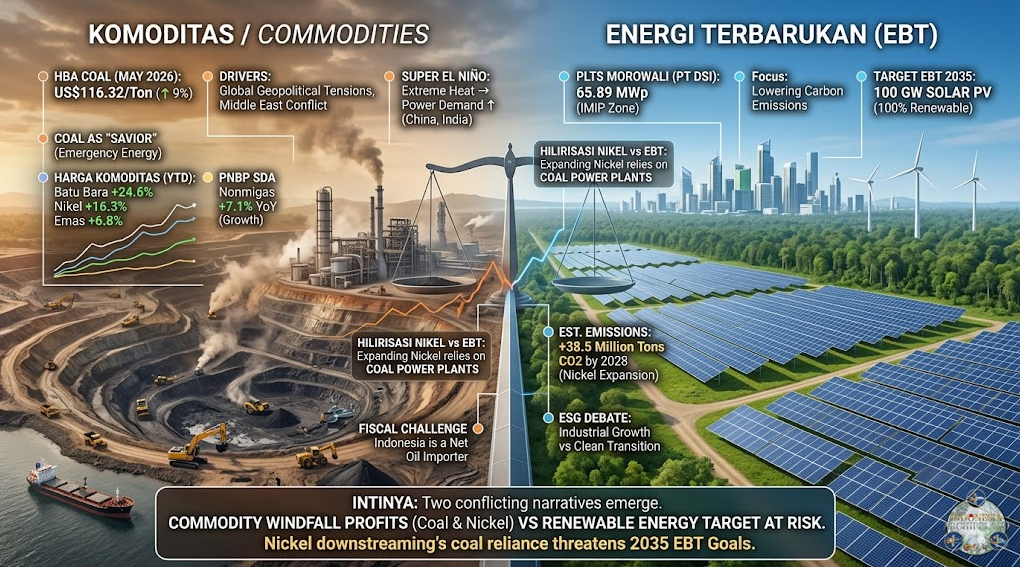

The numbers from May 2026 are instructive. Indonesia's nickel benchmark price, the HMA, moved upward from Period I to Period II of the month, reflecting sustained global demand. Coal benchmark prices told a parallel story: the HBA rose 9 percent to US$116.32 per ton during the same window.

On the ICE Newcastle futures market, coal was trading around US$132 per ton, up 31 percent year-on-year. These are not unrelated figures. They describe the same industrial system from two different angles.

When Extraction Costs the Climate More Than It Saves

Every major nickel smelter expansion in Indonesia requires a reliable, high-capacity power source. The national grid in many nickel-rich regions of Sulawesi and Maluku cannot meet that industrial demand. The practical solution adopted by most smelter operators has been captive coal-fired power plants built adjacent to processing facilities.

The projected carbon consequence of this approach is significant. Nickel downstream expansion in Indonesia is estimated to add 38.5 million tons of CO2 by 2028. That figure represents emissions generated in the course of producing materials that will eventually reduce emissions elsewhere.

The renewable energy share at Indonesia's top nickel smelters currently ranges between 1.2 percent and 30.1 percent depending on the operator, with most sitting far closer to the lower end of that range.

This is not a marginal inefficiency. It is a structural contradiction embedded in the country's industrial development model.

The Benchmark Numbers Behind the Paradox

Understanding why this situation persists requires looking at the commodity environment surrounding it. Coal is not incidental to Indonesia's economy. The country is among the world's largest coal exporters, and elevated coal prices directly benefit state revenues and regional budgets in East Kalimantan, South Kalimantan, and other coal-producing provinces.

When the HBA climbs to US$116.32 per ton and ICE Newcastle futures approach US$132, coal becomes more financially attractive to hold onto domestically as well as to sell.

For smelter operators weighing energy costs, captive coal plants remain the fastest route to reliable industrial-scale power. The economic logic is clear even when the environmental logic is not.

Indonesia's non-oil mineral revenues from PNBP grew 7.1 percent year-on-year, with nickel, coal, and gold all contributing to a commodity windfall that improved fiscal buffers in the first half of 2026. The government has benefited materially from the same resource cycle that is generating the emissions problem.

External Pressures Are Reshaping the Equation

The global energy environment in mid-2026 is adding complexity to an already difficult calculation. Conflict in the Middle East has pushed oil prices past US$108 per barrel, squeezing import-dependent economies. Indonesia is a net oil importer, which means that while the country earns on commodity exports, it absorbs fuel costs on the other side of the ledger.

Japan and Korea, two of the largest buyers of Indonesian nickel products, have begun loosening coal import restrictions to secure domestic power supply in the face of rising electricity demand. UBS has issued Super El Nino warnings pointing to elevated power consumption across Asia in the second half of 2026.

For Indonesia, this means its two most important trading partners for processed nickel are simultaneously more reliant on the same coal that Indonesia is trying to phase out.

This creates an unusual pressure dynamic. On one side, the European Union's carbon border adjustment mechanism is beginning to matter for export-facing Indonesian industries. Battery supply chains sourced from coal-heavy smelters face the prospect of carbon levies that could erode the price advantage Indonesian processors currently hold.

On the other side, key Asian buyers are expanding their own coal use, softening the near-term incentive to invest in cleaner smelting.

What the 2035 Renewable Target Actually Requires

Indonesia has set a national target of 100 gigawatts of solar capacity and 100 percent renewable energy by 2035. Reaching that target alongside continued nickel downstream expansion would require a fundamental shift in how captive industrial power is planned and built.

The math is demanding. Getting the renewable share at nickel smelters from the current range of 1.2 to 30.1 percent to full renewables within nine years means replacing or supplementing gigawatts of coal-fired captive capacity. It means building grid infrastructure into regions where geography has historically made that prohibitively expensive.

it means persuading investors in smelting operations to accept the capital cost of cleaner power when coal remains cheaper in the short term.

Some operators, particularly those with Chinese parent companies supplying battery manufacturers under ESG pressure from European automakers, have begun announcing cleaner energy commitments.

PT Gunbuster Nickel Industry and several facilities under the IMIP complex in Morowali have reported renewable integration milestones. Whether those announcements translate into verified grid data remains a separate question.

The Question That Keeps Getting Deferred

The productive tension in Indonesia's commodity position is not between growth and environment in an abstract sense. It is between who captures the value of the green transition and who absorbs the cost of making it clean. Indonesian policymakers have so far managed this tension by treating nickel downstream expansion and renewable energy targets as parallel tracks that will eventually converge.

The assumption embedded in that approach is that demand for Indonesian battery-grade nickel will remain strong enough, and ESG pressure from end buyers firm enough, to pull smelter operators toward cleaner energy over time without requiring aggressive domestic regulation.

That assumption may hold. Several battery supply chain analysts have pointed to Indonesia as the most likely single-country supplier of processed nickel at scale by the early 2030s. If that position materializes, the leverage Indonesia holds over battery manufacturers could indeed be used to extract clean energy commitments from upstream investors.

But the window for that leverage is not unlimited. Alternative sources of nickel processing capacity are being developed in Canada, Australia, and parts of Southeast Asia. If Indonesian nickel arrives in global markets carrying a documented carbon cost that competitors can undercut, the premium position erodes before the renewable infrastructure is in place.

The coal benchmark rising 9 percent and the nickel HMA climbing in the same month are not separate commodity stories. They are the same industrial story told from two ends of a production chain that has not yet decided which version of itself it wants to export to the world.

The Regulatory Loophole That Keeps Coal in the Game

Indonesia's 2022 energy regulation included a provision that, on the surface, looked like progress. The government prohibited the construction of new coal-fired power plants that had not already been developed and financed. For the national grid, that restriction carried real weight. For the nickel industry, it did not.

The same regulation exempted captive coal plants built to support domestic value addition in mineral processing.

Nickel smelters qualified. The exemption was not an oversight. It reflected a deliberate policy choice to protect the downstream industrialization agenda from energy supply constraints. The consequence is that captive coal capacity linked to nickel processing grew nearly fivefold between 2014 and 2023 and continues to expand.

This is the loophole that makes the 2035 renewable energy target structurally difficult to reach. The coal plants attached to smelters operate outside the national grid managed by PLN. They are private, off-grid, and purpose-built for continuous industrial load.

Because they fall outside PLN's jurisdiction in most planning frameworks, they have historically been excluded from national coal phase-out targets as well.

Integrating them into any credible decarbonization roadmap requires either regulatory revision or a level of investor pressure that has not yet materialized at scale.

The scale of what is being excluded is substantial. In 2023, Indonesia's nickel industry consumed roughly 100 billion kilowatt-hours of electricity. Nearly all of it, close to 97 percent, came from coal-fired plants built and operated by the smelter industry itself.

For every ton of nickel produced under this system, an average of 93 tons of carbon dioxide equivalent is released. That figure makes Indonesian nickel among the most carbon-intensive in the world, measured per unit of output.

A Public Health Cost Embedded in the Industrial Model

The environmental cost of captive coal in nickel production zones is not abstract. It has a documented human dimension that rarely enters commodity pricing discussions. Analysis by the Centre for Research on Energy and Clean Air projects that air pollution from coal-powered smelter hubs could cause 5,000 deaths annually in those regions by 2030, carrying an estimated economic burden of US$3.42 billion per year.

A broader scenario modeling captive coal exclusion from national retirement targets puts the cumulative toll at 27,000 additional air pollution-related deaths and a US$20 billion economic cost before the coal fleet is fully decommissioned.

These numbers represent a transfer of cost. The revenue from nickel exports accumulates at the national level in commodity receipts, PNBP income, and corporate tax. The health and environmental costs concentrate in the communities around smelter complexes in Morowali, Halmahera, and Konawe.

That geographic separation between where the financial benefit accrues and where the physical cost lands is a structural feature of the current model, not a temporary side effect.

Industrial output in nickel processing hubs tends to peak around the fifth year of development. Environmental degradation, by the same modeling, begins to sharply erode economic gains by the eighth year. Several of Indonesia's major nickel processing zones are now entering or approaching that window.

Where Buyer Pressure Is Actually Moving the Needle

The external pressure most likely to drive near-term change is not coming from regulatory reform. It is coming from the end of the supply chain. Mercedes-Benz has committed to carbon neutrality across its entire supply chain by 2039.

Samsung has adopted a policy requiring that all nickel supplied to its manufacturing operations be produced with low or zero emissions.

China, which is both the largest investor in Indonesian smelters and the largest buyer of processed nickel, has signaled through the International Carbon Action Partnership framework that it will move toward limiting purchases of carbon-intensive industrial inputs including steel, aluminum, and by implication, battery materials.

The EU battery passport regulation adds a compliance layer on top of that. From 2026, batteries sold in the EU must be classified based on carbon footprint. From 2027, a maximum lifecycle carbon footprint threshold applies, measured from mineral source through manufacture.

Indonesian nickel processed through coal-powered captive plants carries a carbon intensity that could breach those thresholds. If it does, Indonesian battery-grade nickel loses preferential access to one of the world's largest EV markets precisely at the moment global EV adoption is accelerating.

Indonesian banks have so far not fully absorbed that risk. Five domestic banks have provided financing equivalent to approximately US$1.5 billion to coal-powered smelter and aluminum operations.

Global financial institutions are moving in the opposite direction, with major banks across Asia and Europe withdrawing from coal-fired industrial financing.

The divergence in risk assessment between domestic and international capital creates a financing gap that could widen as carbon compliance requirements tighten.

The Compounding Problem of Competing Timelines

The difficulty Indonesia faces is not a shortage of targets or stated commitments. It is a compounding problem of timelines that do not align with each other. The 2035 renewable energy target is a national planning horizon. The EU battery passport carbon thresholds begin applying in 2027.

Chinese buyer requirements for low-carbon industrial inputs are emerging on a market-driven timeline that no regulatory body controls.

2050 decommissioning deadline for existing industrial coal plants is the backstop, but by the time that deadline arrives, the competitive position Indonesia is trying to protect in the global battery supply chain will have been settled years earlier.

That gap between when the compliance pressure arrives and when the infrastructure transition is scheduled to complete is where Indonesia's commodity paradox is most acute.

The country is building downstream nickel capacity at a pace the energy transition genuinely needs, using an energy source the energy transition is designed to eliminate, on a decarbonization schedule that trails the market requirements it is trying to meet.

The commodity benchmarks from May 2026 capture a moment in that trajectory. Rising nickel prices reflect genuine global demand for the material at the center of the clean energy shift. Rising coal prices reflect the cost of producing it.

Both lines are moving upward at the same time because they are part of the same system. Whether Indonesia can separate those two trends before the market does it for them is the industrial policy question that the benchmark numbers alone cannot answer.